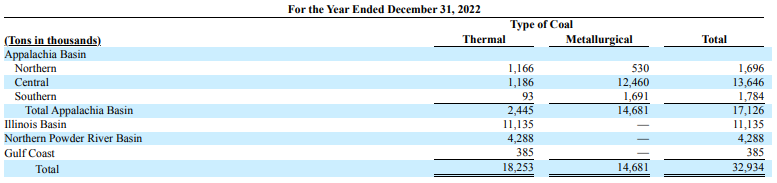

Editor’s note: This is the latest edition in the “Company Notes Series”, where we periodically share our notes on companies we’ve studied in the recent past but currently have no vested interest in (we may invest in or sell shares in the companies mentioned at any time). The notes are raw and not updated, and the “as of” date for the data is given at the start of the notes. The first three editions in the series can be found here, here, and here. Please give us your thoughts on the series through the “Contact Us” page; your feedback will determine if we continue with it. Thanks in advance!

Start of notes for engcon

Data as of 31 December 2023

Background

- Year founded: 1990

- Listed in Stockholm Stock Exchange (Sweden) since 17 June 2022

- Headquarters: Stromsund, Sweden

Business

- engcon manufactures tiltrotator systems that turns excavators into tool carriers (see Figure 1). The hydraulic tools provided by the company include detachable grippers, stone and sorting grabs, combi grabs, and more. See engcon’s Youtube video for more.

- engcon’s tiltrotator solutions are developed, manufactured and subsequently fitted on new or existing excavators. Dealers serve as a link between excavator manufacturers (OEMs, or original equipment manufacturers), tiltrotator manufacturers, and end-customers. End-customers are contractors, companies that own excavators, and excavator rental companies. engcon has partnerships with OEMs that increase the reach of the company’s products and prepare excavators for faster and easier installations of tiltrotators; the partnerships also provide valuable insight into which technologies OEMs are developing for the future, and engcon contributes with knowledge of end-customer requirements.

- engcon’s tiltrotator solutions are focused on excavators in the weight class of 2 tonnes to 33 tonnes.

- The production of engcon’s tiltrotator solutions happens in the company’s production sites in Strömsund, Sweden and Niepruszewo, Poland. engcon’s tiltrotator solutions consist of various components designed by the company. Some of the components are also manufactured at engcon’s aforementioned production sites but most of the components are purchased from suppliers in Sweden and Northern Europe.

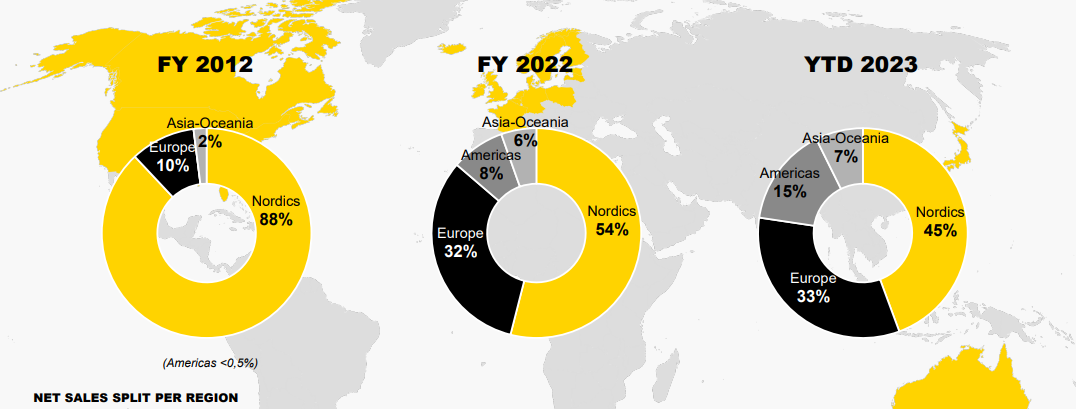

- engcon had sales in 16 markets across the globe in 2022 and its sales split by geographic region in 2022 and 9M 2023 is shown in Figure 2 below. The years in which engcon entered its various markets are:

- Sweden: 1990

- Finland and Norway: 1995

- Denmark and Germany: 2003

- UK: 2004

- France: 2014

- Netherlands: 2016

- USA: 2017

- Japan: 2018

- South Korea and Australia: 2020

- Canada, Belgium, Ireland, and Austria: 2021-2022

- The majority of engcon’s sales take place through a global network of dealers. Sales also take place through collaboration with OEM dealer networks. A limited amount of products, mainly buckets and tools, are sold through engcon’s website in Sweden, Finland and Denmark.

- No single customer accounted for >10% of engcon’s sales in 2022, so there’s no customer concentration. But there may be supplier concentration for engcon: 10 of engcon’s largest suppliers in 2021 accounted for 58% of the company’s total purchases of raw materials and components.

- A tiltrotator had an average price (including engcon and competitors) of SEK 176,000 (around US$19,000) in 2021. Dealers typically earn 30% of the price of a tiltrotator.

- engcon released its 3rd-gen tiltrotator solution in May 2022. The 3rd-gen system is equipped with technology that has never been used on tiltrotators and that takes a clear step towards the electrified, connected and autonomous excavators of the future. The 3rd-gen’s load-sensing technology leads to reduced fuel consumption, improved precision, less wear and tear, and lower maintenance costs. The reduced energy need simplifies the use of alternative fuels for excavators, such as electricity and hybrid solutions. With help from a new sensor technology, the newly developed control system can precisely calculate the tilt and rotation of the tiltrotator, which means improved user-friendliness and greater potential for autonomous operations. Furthermore, the newly developed control system enables a more efficient remote connection, thereby improving remote support as well as the ability to remotely configure equipment.

Market opportunity

Newly manufactured excavator market for engcon

- Globally, 665,000 excavators were sold in 2021. Of these 665,000 excavators, a total of 181,775 excavators belonging to the 2-33 tonne weight class (engcon’s focus is on excavators in that weight class) were sold in the Nordics, Europe, Americas, and Asia/Oceania; these regions are engcon’s key geographical markets as shown in Figure 2, and are named as the Focus Markets by the company. In the same year (2021), 12,934 tiltrotators for newly manufactured excavators, and 1,750 tiltrotators for existing excavators, were sold. The value of the tiltrotators sold was SEK 2.6 billion (around US$285 million).

- The number of excavators sold in the Focus Markets compounded at 6% per year for 2016-2019. COVID affected the market in 2020, but ultimately, the number of excavators sold in the Focus Markets still compounded at 2% per year for 2016-2021. The historical growth in the excavator market for each of engcon’s Focus Markets:

- Nordic: 7,206 excavators sold in 2021, CAGR (compound annual growth rate) of 3% for 2016-2019, CAGR of 1% for 2016-2021,

- Europe: 76,097 excavators sold in 2021, CAGR of 6% for 2016-2019, CAGR of 2% for 2016-2021

- Americas: 62,972 excavators sold in 2021, CAGR of 10% for 2016-2019, CAGR of 4% for 2016-2021

- Asia/Oceania: 35,481 excavators sold in 2021, CAGR of 2% for 2016-2019, CAGR of -1% for 2016-2021

- The number of tiltrotators sold in the Focus Markets had a CAGR of 11% for 2016-2021, including a 15% decline in 2020 because of COVID. The value of tiltrotators sold in the Focus Markets had a CAGR of 15% for 2016-2021.

- According to PwC, the value of the tiltrotators market is expected to compound at 19% from 2021 to 2026, driven by: (1) greater demand for productivity increases; (2) population growth and urbanisation; (3) lack of labour; (4) sustainability requirements; (5) excavators transitioning to becoming multi-purpose tool carriers and more autonomous; (6) and digitalisation and electrification of the construction market.

- According to PwC: (1) Excavators equipped with tiltrotators are able to replace 2.2 other construction machines on average; (2) a tiltorator can increase the productivity of an excavator by 25%; (3) the use of a tiltrotator can save 6,000 litres of diesel annually, thus reducing 16,200 kg of CO2 emissions per year; (4) excavators with tiltrotators have a better safety profile as operators can exchange tools from within the cabin.

- The penetration rate of tiltrotators in newly manufactured excavators was 2% globally in 2021, 85% in the Nordics (92% in Sweden), and 7% in the Focus Markets. The penetration rate is closely connected to the maturity of the market, which can be divided into 3 phases: Development; acceleration; and mature. In the development phase, the penetration rate increases from 0% to 20%-25%. In the acceleration phase, the penetration rate has passed 20% and risen to 60%. The tipping point between the development phase and the acceleration phase is where the tiltrotator takes the step to becoming an established market standard. Authorities and clients, such as major construction and civil engineering companies, places requirements on excavators to be equipped with a tiltrotator for efficiency and safety reasons. Once the tipping point has been reached, the sales of tiltrotators to both new excavators and the aftermarket tends to gain momentum.

- The market for tiltrotator manufacturers has 5 major operators (see Figure 3) that account for 95% of sales. engcon is the largest, with a market share of 45%. Tiltrotator manufacturers can be divided into 4 groups: global manufacturers, local manufacturers, other operators whose core operations are not tiltrotators, and excavator manufacturers (OEMs) with in-house manufactured tiltrotators. The 5 largest tiltrotator manufacturers are all global manufacturers, 4 of which are Swedish. All 5 collaborate with OEMs and the product portfolio includes quick couplers, tools, and other advanced attachments for excavators. engcon’s market share has increased from 42% in 2019 and 43% in 2020.

Existing excavator market for engcon

- Number of newly-manufactured excavators in engcon’s Focus Markets that will not be equipped with tiltrotators for 2022-2026 is expected to be 960,000. This provides a large pool of retrofitting potential for engcon.

Management and major shareholders

- engcon has Class A and Class B shares. Class A shares carry 10 votes per share while Class B shares have 1 vote per share. The Class B shares are public-listed. At end-2022, engcon had a total sharecount of 151.788 million (35.34 million Class A shares, 116.44 million Class B shares.

- Stig Engstrom, 62, is the founder of engcon. He handed over the CEO role to Orjan Westerlund in 2003, and has been on the board of engcon since. Stig Engstrom controlled 29.04 million Class A shares and 24.74 million Class B shares at end-2022, which amounted to 35.4% of engcon’s total share count, but 67.1% of the total votes.

- Stig Engstrom’s ex-wife, Monica Engstrom, has been on engcon’s board since 2004. Monica Engstrom controlled 6.31 million Class A shares and 42.21 million Class B shares at end-2022, which amounted to 32.0% of engcon’s total share count, but 22.4% of the total votes.

- engcon’s CEO is Krister Blomgren, 58, who has been in the role since 2011. Blomgren controlled 1.259 million engcon Class B shares as of end-2022, which is 0.8% of the total share count.

- Other members of engcon’s management team are shown in Table 1 below (some of them have long tenures, which is good):

- Remuneration of Stig Engstrom and Krister Blomgren for 2019-2022 is shown in Table 2 below. Not much details are given on how they are compensated beyond the total amounts. The big jump in compensation for Blomgren in 2022 bears watching, but is only a tiny percentage of engcon’s profit and cash flow during the year.

Financials

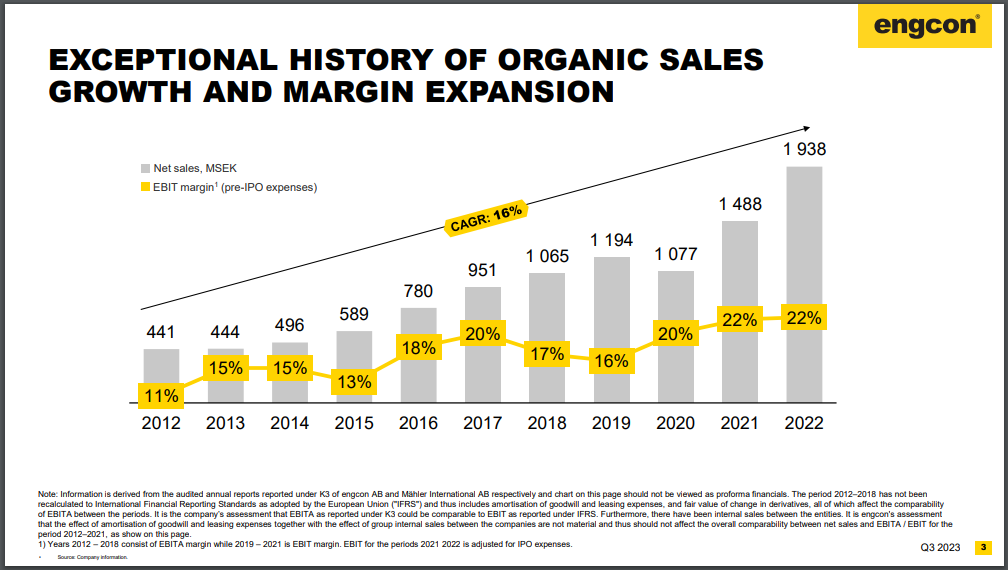

- engcon’s revenue has CAGR of 16% from 2012 to 2022, and EBIT margin has doubled from 11% to 2022% in that period. See Figure 4

- From Table 3 above, engcon’s revenue CAGR for 2019 to 12 months ended 30 Sep 2023 is 16.7%. Net income CAGR is 25.6%, and FCF CAGR is 44.8%. Average net income margin is 15.9%, and average FCF margin is 14.0%.

- engcon saw a large pull-forward of orders in 2021 Q4 and 2022 Q1, mainly in Nordic and Europe, due to price increases and uncertainty concerning delivery times, combined with an uncertain business environment and long lead times. So engcon expects 2023’s overall revenue growth to be just 8% (2023 Q1 growth was 55%, 2023 Q2 was -5%, and 2023 Q3 was -6%). Operating income also fell sharply in 2023 Q2 (12%) and 2023 Q3 (51%)

Valuation

- Stock price on 31 December 2023: SEK 93.30

- Trailing EPS = 2.33; Trailing PE = 40

- Trailing FCF per share = 2.80; trailing PFCF = 33

- For a company that is very likely going to post a further year-on-year decline in net income and FCF in 2023 Q4, those valuations look high.

Risks

- engcon protects its business via patents, of which the most important relates to EC-Oil, which is a quick coupler system that allows for the replacement of hydraulic tools from the excavator’s cabin without the mounting of hoses and electrical cables. The patent, which has a maximum validity up to and including 2024, is not assessed to be business-critical, but it still helps to distinguish engcon’s tiltrotator systems and make it more difficult for competitors to copy. When the patent for EC-Oil expires, it may be difficult for engcon to have a distinctive product offering.

- The sale of excavators globally has been stronger than what I expected before researching engcon. But the overall construction market – including the sale of excavators – is probably sensitive to recessions. So future recessions are a risk.

- There’s the possibility that someone comes up with a superior tiltrotator or similar solution to what engcon has.

- In the shorter term, engcon has clearly been over-earning in 2021 and 2022, and is now suffering the hangover in 2023. Will the hangover last a long time? That’s a possibility, despite tiltrotators being a superior solution.

- In June 2022, Rototilt Group filed a lawsuit against engcon that alleged that the company had infringed upon a patent. The adjusted damages claimed amounted to approximately SEK 200 million. The alleged infringement relates to sensor technology in the Q-safe locking system. In May 2023, the Swedish Patent and Market Court announced its verdict regarding Rototilt’s lawsuit against engcon. The court determined that no infringement had taken place and therefore dismissed Rototilt’s action. The court determined that no infringement had taken place and therefore dismissed Rototilt’s action. At the same hearing, engcon claimed that Rototilt’s patent should be declared invalid. However, the court determined that the patent was valid. Following appeals, both parties were granted leave to appeal by the Swedish Patent and Market Court. A ruling in the higher court is expected in spring 2024 at the earliest.

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. We currently have no vested interest in any company mentioned. Holdings are subject to change at any time.