Economist Richard Koo (Gu Chao Ming) is the author of the book The Other Half of Macroeconomics and the Fate of Globalization. Investor Li Lu published a Mandarin review of the book in November 2019, which I translated into English in March 2020. When I translated Li’s review, I found myself nodding in agreement to Koo’s unique concept of a balance sheet recession as well as his analyses of Japan’s economic collapse in the late 1980s and early 1990s, and the Japanese government’s responses to the crash.

When I realised that Koo was interviewed last week in an episode of the Bloomberg Odd Lots podcast to discuss the Chinese government’s recent flurry of stimulus measures, I knew I had to tune in – and I was not disappointed. In this article, I want to share my favourite takeaways (the paragraphs in italics are transcripts from the podcast)

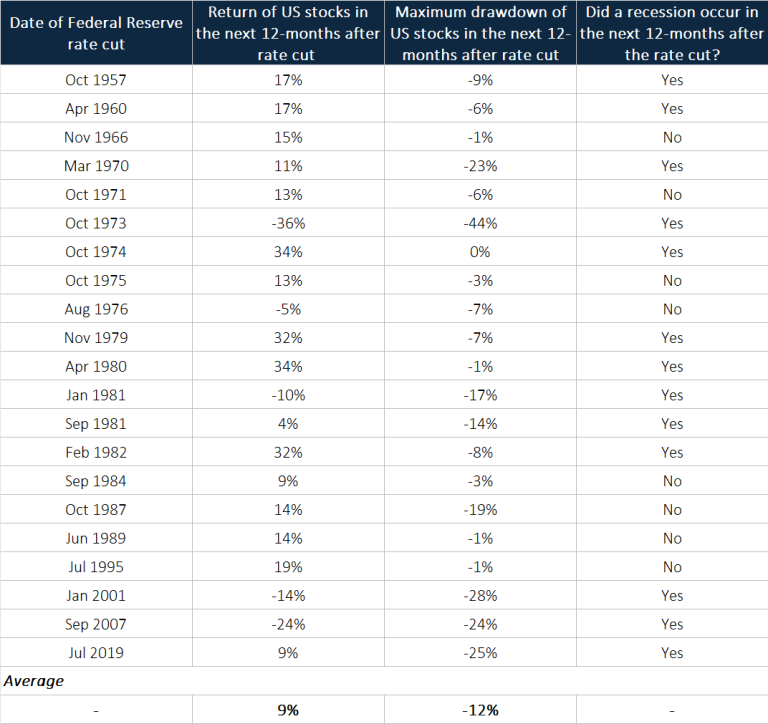

Takeaway #1: China is currently facing a balance sheet recession, and in a balance sheet recession, the economy can shrink very rapidly and be stuck for a long time

I think China is facing balance sheet recession and balance sheet recession happens when a debt-financed bubble bursts, asset prices collapse, liabilities remain, people realise that their balance sheets’ under water or nearly so, and they all try to repair their balance sheets all at the same time…

…Suppose I have $1000 of income and I spend $900 myself. The $900 is already someone else’s income so that’s not a problem. But the $100 that I saved will go through people like us, our financial institutions, and will be lent to someone who can use it. That person borrows and spends it, then total expenditure in economy will be $900 that I spent, plus $100 that this guy spent, to get $1000 against original income of $1000. That’s how economy moves forward, right? If there are too many borrowers and economy is doing well, central banks will raise rates. Too few, central bank will lower rates to make sure that this cycle is maintained. That’s the usual economy.

But what happens in the balance sheet recession is that when I have $1000 in income and I spend $900 myself, that $900 is not a problem. But the $100 I decide to save ends up stuck in the financial system because no one’s borrowing money. And China, so many people are refusing to borrow money these days because of that issue. Then economy shrinks from $1000 to $900, so 10% decline. The next round, the $900 is someone else’s income, when that person decides to save 10% and spends $810 and decides to save $90, that $90 gets stuck in the financial system again, because repairing financial balance sheets could take a very long time. I mean, Japanese took nearly 20 years to repair their balance sheets.

But in the meantime, economy can go from $1000, $900, $810, $730, very, very quickly. That actually happened in United States during the Great Depression. From 1929 to 1933, the United States lost 46% of its nominal GDP. Something quite similar actually happened in Spain after 2008when unemployment rates skyrocketed to 26% in just three and a half years or so. That’s the kind of danger we face in the balance sheet recession.

Takeaway #2: Monetary policy (changing the level of interest rates) is not useful in dealing with a balance sheet recession – what’s needed is fiscal policy (government spending), but it has yet to arrive for China

I’m no great fan of using monetary policy, meaning policies from the central bank to fight what I call a balance sheet recession…

…Repairing balance sheets of course is the right thing to do. But when everybody does it all at the same time, we enter the problem of fallacy of composition, in that even though everybody’s doing the right things, collectively we get the wrong results. And we get that problem in this case because in the national economy, if someone is repairing balance sheets, meaning paying down debt or increasing savings, someone has to borrow those funds to keep the economy going. But in usual economies, you bring interest rates down, there’ll be people out there willing to borrow the money and spend it. That’s how you keep the economy going.

But in the balance sheet recession, you bring interest rates down to very low levels – and Chinese interest rates are already pretty low. But even if you bring it down to zero, people will be still repairing balance sheets because if you are in negative equity territory, you have to come out of that as quickly as possible. So when you’re in that situation, you cannot expect private sector to respond to lowering of interest rates or quantitative easing, forward guidance, and all of those monetary policy, to get this private sector to borrow money again because they are all doing the right things, paying down debt. So when you’re in that situation, the economy could weaken very, very quickly because all the saved funds that are returned to the banking system cannot come out again. That’s how you end up with economy shrinking very, very rapidly.

The only way to stop this is for the government, which is outside of the fallacy of composition, to borrow money. And that’s the fiscal policy of course, but that hasn’t come out yet. And so yes, they did the quick and easy part with big numbers on the monetary side. But if you are in balance sheet recession, monetary policy, I’m afraid is not going to be very effective. You really need a fiscal policy to get the economy moving and that hasn’t arrived yet.

Takeaway #3: China’s fiscal policy for dealing with the balance sheet recession needs to be targeted, and a good place to start would be to complete all unfinished housing projects in the country, followed by developing public works projects with a social rate of return that’s higher than Chinese government bond yields

If people are all concerned about repairing their balance sheets, you give them money to spend and too often they just use it to pay down debt. So even within fiscal stimulus, you have to be very careful here because tax cuts I’m afraid, are not very effective during balance sheet recessions because people use that money to repair their balance sheets. Repairing balance sheets is of course the right thing to do, but it will not add to GDP when they’re using that tax cuts to pay down debt or rebuild their savings. So that will not add to consumption as much as you would expect under ordinary circumstances. So I would really like to see government just borrow and spend the money because that will be the most effective way to stop the deflationary spiral…

… I would use money first to complete all the apartments that were started but are not yet complete. In that case you might have to take some heavy handed actions, but basically the government should take over these companies and the projects, and start putting money so that they’ll complete the projects. That way, you don’t have to decide what to make, because the things that are already in the process of being built – or the construction drawings are there, workers are there, where to get the materials. And in many cases, potential buyers already know. So in that case, you don’t waste time thinking about what to build, who’s to design, and who the order should go to.

Remember President Obama, when he took over 2009, US was in a balance sheet recession after the collapse of the housing bubble. But he was so careful not to make the Japanese mistake of building bridges to nowhere and roads to nowhere. He took a long time to decide which projects should be funded. But that year-and-a-half or so, I think the US lost quite a bit of time because during that time, economy continued to weaken. There were no shovel-ready projects.

But in the Chinese case, I would argue that these uncompleted apartments are the shovel-ready projects. You already know who wants them, who paid their down payments and all of that. So I will spend the money first on those projects, complete those projects, and use the time while the money is used to complete these apartments.

I would use the magic wand to get the brightest people in China to come into one room and ask them to come up with public works projects with a social rate of return higher than 2.0%. The reason is that Chinese government bond is about 2.00-something. If these people can come up with public works projects with a social rate of return higher than let’s say 2.1%, then those projects will be basically self-financing. It won’t be a burden on future taxpayers. Then once apartments are complete, then the economy still is struggling from balance sheet recession, then I would like to spend the money on those projects that these bright people might come up with.

Takeaway #4: The central government in China actually has a budget deficit that is a big part of the country’s GDP, unlike what official statistics say

But in China, even though same rules should have applied, local governments were able to sell lots of land, make a lot of money in the process, and then they were able to do quite a bit of fiscal stimulus, which also of course added to their GDP. That model will have to be completely revised now because no one wants to buy land anymore. So the big source of revenue of local governments are gone and as a result, many of them are very close to bankrupt. Under the circumstances, I’m afraid central government will have to take over a lot of these problems from the local government. So this myth that Chinese central government, the budget deficit is not a very big part of GDP, that myth will have to be thrown out. Central government will have to take on, not all of it perhaps, but some of the liabilities of the local governments so that local governments can move forward.

Takeaway #5: There’s plenty of available-capital for the Chinese central government to borrow from, and the low yields of Chinese government bonds are a sign of this

So even though budget deficit of China might be very large, the money is there for government to borrow. If the money is not there for the government to borrow, Chinese government bond yields should have gone up higher and higher. But as you know, Chinese government 10-year government bond yields almost down to 2.001% or 2%. It went that low because there are not enough borrowers out there. Financial institutions have to place this money somewhere, all these deleveraged funds coming back into the financial institutions, newly generated savings, all the money that central bank put in, all comes to basically people like us in the financial institutions, the fund managers. But if the private sector is not borrowing money, the only borrower left is the government.

So even if the required budget deficit might be very large to stabilize the economy, the funds are available in the financial market. Only the government just have to borrow that and spend it. So financing should not be a big issue for governments in balance sheet recession. Japan was running huge budget deficits and a lot of conventional minded economists who never understood the dynamics of balance sheet recession was warning about Japan’s budget deficit growing sky high, and then interest rates going sky high. Well, interest rates kept on coming down because of the mechanism that I just described to you, that all those funds coming into the financial sector cannot go to the private sector, end up going to our government bond market. And I see the same pattern developing in China today.

Takeaway #6: Depending on exports is a great way for a country to escape from a balance sheet recession, but this route is not available for China because its economy is already running the largest trade surplus in the world

Export is definitely one of the best ways if you can use it, to come out of balance sheet recession. But China, just like Japan 30 years ago, is the largest trade surplus country in the world. And if the world’s largest trade surplus country in the world tries to export its way out, very many trading partners will complain. You are already such a large destabilizing factor on the world trade, now you’re going to destabilize it even more.

I remember 30 years ago that United States, Europe, and others were very much against Japan trying to export its way out. Because of their displeasure, particularly the US displeasure, Japanese yen, which started at 160 yen when the bubble burst in 1990, ended up 80 yen to the dollar, five years later, 1995. What that indicated to me was that if you’re running trade deficit, you can probably export your way out and no one can really complain because you are a deficit country to begin with. But if you are the surplus country, and if you’re the largest trade surplus country in the world, there will be huge pushback against that kind of move by the Chinese. We already seeing that, in very many countries complaining that China should not export its problems.

Takeaway #7: Regulatory uncertainties for businesses that are caused by the Chinese central government may have played a role in the corporate sector’s unwillingness to borrow

Aside from a balance sheet recession, which is a very, very serious disease to begin with, we have those other factors that started hurting the Chinese economy, I would say, starting as early as 2016.

When you look at the flow of funds data for the Chinese economy, you notice that the Chinese corporate sector started reducing their borrowings, starting around 2016. So until 2016, Chinese companies were borrowing all the household sector savings generated, which is of course the ideal world. The household sector saving money, the corporate sector borrowing money. But starting around 2016, you see corporate sector borrowing less and less. And at around the Covid time, corporate sector was actually a net saver, not a net borrower. So that trend, I think has to do with what you just described, that regulatory uncertainties got bigger and bigger under the current leadership and I think people began to realize that even after you make these big investments in the new projects, they may not be able to expect the same revenue stream that they expected earlier because of this regulatory uncertainty.

Takeaway #8: China’s economy was already running a significant budget deficit prior to the bubble bursting, and this may have made the central government reluctant to step in as borrower of last resort now to fix the balance sheet recession

If the household sector is saving money, but the corporate sector is not borrowing money, you need someone else to fill that gap. And actually that gap was filled by Chinese government, mostly decentralized local governments. But if that temporary fiscal jolt of fiscal stimulus then turn the economy around, then those local government interventions would’ve been justified. But because this was a much more deeply rooted – here, I would use structural problems, this regulatory uncertainties and middle income trap and so forth – local government just had to keep on borrowing and spending money to keep the economy going. That was happening long before the bubble burst. So if you look at total, or what I call general government spending – not just the central government, but the general government – they were financial deficit to the tune of almost 7% of GDP by 2022. This is before the bubble bursting.

So if you are already running a budget deficit, 7% of GDP before the onset of balance sheet recession, then whatever you have to do to stop balance sheet recession, we have to be on top of the 7%. Suppose you need 5% GDP equivalent to keep the economy going, then you’re talking about 12% of GDP budget deficit. I think that’s one of the reasons why Chinese policy makers, even though many of them are fully aware that in the balance sheet recession, you need the government to come in, they haven’t been able to come to a full consensus yet because even before the bubble burst, Chinese government was writing a large budget deficit.

Disclaimer: The Good Investors is the personal investing blog of two simple guys who are passionate about educating Singaporeans about stock market investing. By using this Site, you specifically agree that none of the information provided constitutes financial, investment, or other professional advice. It is only intended to provide education. Speak with a professional before making important decisions about your money, your professional life, or even your personal life. I don’t have a vested interest in any company mentioned. Holdings are subject to change at any time.